Does your financial life feel like a constant game of catch-up? You tell yourself you’ll start saving “next month,” or that you’ll finally make a budget, but it never seems to happen. You’re not bad with money—you just haven’t built the right systems yet. The good news? Transforming your finances isn’t about complex math or willpower; it’s about rewiring your daily routines. This guide will show you how to build powerful money habits that automate success, reduce stress, and finally align your spending with your deepest goals. Let’s create a financial life you don’t need a vacation from.

What Are “Money Habits” Really?

Let’s start by demystifying the term. Money habits aren’t just about budgeting or saving. They are the automatic, often unconscious, financial behaviors you perform every single day. They’re the reason you grab a coffee without thinking, scroll through a shopping app when you’re bored, or feel that pang of anxiety when you check your bank account.

Think of your brain as a path through a forest. The more you walk the same route, the clearer and easier the path becomes. Your current financial behaviors are like well-worn trails. The goal isn’t to suddenly forge a new path through thick brambles through sheer force of will. It’s to start walking a new, better path consistently until it becomes the default, easy route. A money habit can be as simple as checking your account balance each morning, automatically transferring $5 to savings with every paycheck, or meal planning every Sunday to avoid costly takeout. It’s the small, repeated action that creates monumental change over time.

Why Do Money Habits Matter So Much?

You might think financial success comes from one big move—getting a raise, a lucky investment, or winning the lottery. But the truth is, your long-term financial health is determined by the small, daily choices you make consistently. Your money habits are the compound interest of behavior.

Without good habits, even a high income can vanish. With strong habits, even a modest income can build into significant wealth and security. This matters because money isn’t just about numbers in an account; it’s about freedom. It’s the freedom to choose a job you love, to handle an emergency without panic, to provide for your family, and to sleep soundly at night. Good money habits build the foundation for that freedom. They move you from reacting to financial fires to proactively designing a life you’re excited to live.

How the Habit-Building Process Actually Works

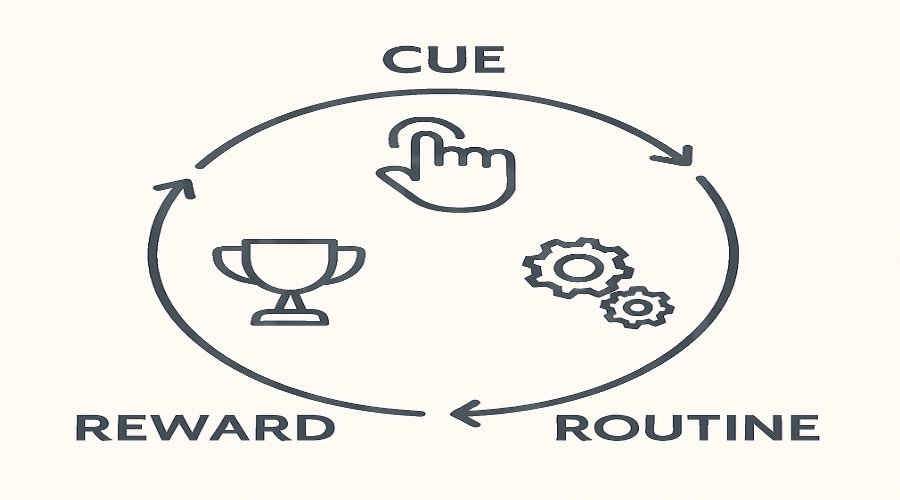

To build better money habits, it helps to understand the neurological loop that creates any habit. It’s a simple three-part cycle that, once mastered, you can use to your advantage:

- The Cue: This is the trigger that starts the behavior. It can be a time of day (morning), an emotional state (boredom or stress), a location (passing your favorite coffee shop), or a preceding action (sitting down on the couch).

- The Routine: This is the behavior itself—the action you take. This is the habit you’re trying to change, like ordering takeout or making an impulse online purchase.

- The Reward: This is the positive feeling or benefit you get from the behavior. It provides the reinforcement that makes your brain want to repeat the loop. The reward might be a sugar rush, a temporary feeling of relief from boredom, or the thrill of a new purchase.

The key to building better money habits is not to eliminate the loop, but to hack it. You identify the cue and the reward, and then you swap in a new, healthier routine that delivers a similar reward. The cue (feeling bored) might currently lead to the routine (online shopping) for the reward (a dopamine hit). Your new loop could be: Cue (feeling bored) -> Routine (researching a free hobby or going for a walk) -> Reward (a dopamine hit and a sense of accomplishment).

The Incredible Benefits of Mastering Your Money Habits

When you start deliberately shaping your financial routines, the rewards extend far beyond your bank balance. You’ll experience a cascade of positive effects.

- Drastic Reduction in Financial Stress: This is the most immediate and profound benefit. When you have systems in place, that background hum of money anxiety simply vanishes. You know where your money is going, you’re prepared for surprises, and you’re actively working toward your goals.

- Automated Progress Toward Goals: Good habits turn massive, daunting goals (like “save $20,000”) into small, automatic actions (“transfer $100 every Friday”). You make progress without having to constantly think about it or exert willpower.

- Improved Decision-Making: With a clear financial framework, daily spending decisions become effortless. You have a simple litmus test: “Does this align with my goals and my plan?” This eliminates decision fatigue and buyer’s remorse.

- Stronger Relationships: Money is a leading cause of stress in relationships. When you build healthy money habits as a team—or even just improve your own—it reduces conflict and builds a foundation of trust and shared purpose.

- A Sense of Empowerment: Taking active, consistent control of your finances is one of the most empowering things you can do. It builds confidence that spills over into every other area of your life.

The 5 Most Common Money Habit Mistakes (And How to Avoid Them)

We all stumble when trying to build new routines. I’ve made every one of these mistakes myself. Here’s how to sidestep them.

- Mistake #1: Trying to Change Everything at Once. You get motivated and decide to start budgeting, cutting all subscriptions, cooking every meal, and saving 50% of your income, all starting Monday. This is a recipe for burnout and failure.

- The Fix: Start with ONE habit. Just one. Master it for a few weeks before even considering adding another.

- Mistake #2: Being Too Restrictive. If your new habit feels like a punishment, your brain will rebel. A budget with zero “fun money” or a plan that eliminates all your small joys will not last.

- The Fix: Build guilt-free spending into your plan. Sustainable money habits include room for life and enjoyment.

- Mistake #3: Not Tracking Your Progress. If you don’t measure it, you can’t manage it. Without tracking, it’s easy to forget your new habit and lose motivation.

- The Fix: Use a simple habit tracker (an app or a paper calendar) and give yourself a checkmark for every day you complete your new habit. This visual proof of progress is incredibly motivating.

- Mistake #4: Not Linking the Habit to a Deeper “Why.” “Saving money” is a vague goal. “Saving money for a down payment so I can have a backyard for my dog” is a powerful motivator.

- The Fix: Dig deep. Ask yourself why you want to build this habit. Connect it to your values and your vision for your ideal life.

- Mistake #5: Beating Yourself Up Over Slip-Ups. You miss a day or have a bad week. The old narrative says, “I’ve failed, I might as well give up.”

- The Fix: Treat a mistake as data, not failure. Ask, “What caused the slip-up? How can I adjust my environment or routine to make it easier next time?” Then, just get back on track with the very next decision.

Your Step-by-Step Guide to Building Better Money Habits

Ready to build habits that stick? Follow this actionable, progressive plan. Remember, the goal is progress, not perfection.

Phase 1: The Foundation (Weeks 1-2)

Step 1: Conduct a No-Judgment Financial Audit.

For one week, your only job is to observe. Track every single dollar that comes in and goes out. Use an app, a notes file on your phone, or a small notebook. Do not try to change anything yet. The goal here is awareness. You’re gathering data about your current “paths” so you know which ones need redirecting. You’ll likely discover a few “wow” moments—small expenses that add up to a shocking amount.

Step 2: Define Your “Big Why.”

Grab a journal and answer these questions:

- What does financial freedom look and feel like to me?

- What would I do if I had zero money stress?

- What is one specific, exciting goal I want to achieve in the next year? (e.g., a vacation, paying off a credit card, building a $1,000 emergency fund).

Write your “Big Why” on a notecard and put it somewhere you’ll see it daily. This is your anchor.

Phase 2: Building Your Core Habit Stack (Weeks 3-6)

Step 3: Start with ONE “Keystone” Habit.

Choose one habit that will have an outsized positive impact. Don’t start with the hardest one. Pick the one that feels most achievable. Great starter habits include:

- The 5-Minute Daily Money Check-In: Every morning with your coffee, open your banking app and look at your balances. Don’t judge, just observe.

- Automate a Tiny Savings Transfer: Set up an automatic transfer of $10-$20 to your savings account to happen the day after you get paid.

- The “List” Rule: Commit to not making any online purchase without first adding it to a list and waiting 24 hours.

Step 4: Engineer Your Environment for Success.

Make your good habit easier and your bad habits harder.

- To save more: Set up the automatic transfer (easy) and delete shopping apps from your phone (hard).

- To spend less on food: Plan your meals for the week and do a grocery pickup order (easy) and unsubscribe from food delivery service emails (hard).

- To check your accounts: Put a sticky note on your coffee maker that says “Check-in!” (cue).

Step 5: Track and Celebrate.

Get a habit tracker. For every day you complete your one new habit, give yourself a checkmark. After one full week of success, celebrate with a non-financial reward—watch a movie, take a long bath, whatever feels good to you. This links positive emotion to your new behavior.

Phase 3: Scaling and Solidifying (Weeks 7+)

Step 6: “Stack” Your Next Habit.

Once your first habit feels automatic (like brushing your teeth), it’s time to add another. Use a technique called “habit stacking.” Link your new habit to an existing one. The formula is: “After I [Current Habit], I will [New Habit].”

- Example: “After I check my bank balance each morning, I will transfer any ‘leftover’ money from yesterday’s budget to my savings.” (e.g., if you budgeted $15 for lunch but only spent $12, you transfer $3).

Step 7: Perform a Monthly “Money Date.”

Once a month, schedule a 30-minute meeting with yourself (and your partner, if applicable). Put on some music, grab a drink, and review your progress. Look at your spending, celebrate your wins, and adjust your habits and goals for the next month. This turns money management from a chore into an act of self-care.

“the r/Frugal subreddit“

Step 8: Gradually Increase the Challenge.

As your habits become ingrained, slowly increase the difficulty to match your growing skill. If you started by saving $10 a week, can you make it $15? If you’ve mastered tracking your spending, can you create a simple 50/30/20 budget? The constant, slight challenge keeps you engaged and progressing.

Your New Financial Life Awaits

Building better money habits is a journey of a thousand small steps, not one giant leap. It’s about being kind to yourself, consistent in your actions, and always connected to your “why.” You are not just moving decimal points around a screen; you are building a life of less stress, more freedom, and greater choice.

You now have the map. You understand the psychology, you’ve seen the common pitfalls, and you have a clear, step-by-step plan. The power to transform your financial reality is in your hands, and it starts with one single, small habit.

Your first step is simple. Don’t try to do it all. Just choose ONE of the starter habits from Step 3 and commit to doing it for the next seven days. That’s it. The rest will follow. Your future, financially-empowered self is waiting—go and make them proud.